An inventory reserve is a contra-asset account used to write down the reported value of inventory, reflecting estimated losses from obsolescence, spoilage, theft, or market price decline before specific items are identified.

This guide covers reserve mechanics and journal entries, causes of inventory value loss, calculation methods, financial statement placement and compliance standards, and the role of unified inventory data in reducing estimation errors.

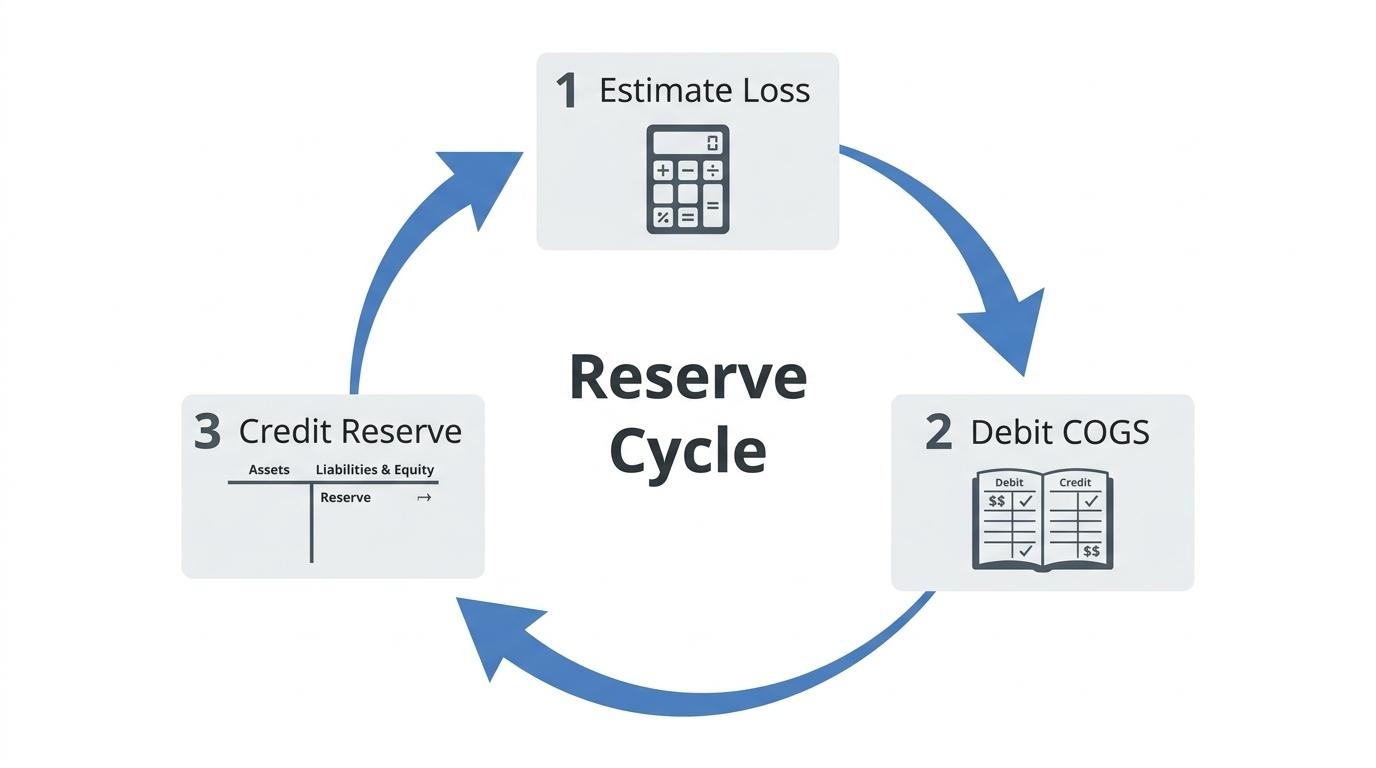

Reserve mechanics follow a clear cycle: businesses estimate a loss percentage or dollar amount, debit Cost of Goods Sold, and credit the contra-asset account on the balance sheet. Each reporting period, the estimate is revised based on shrinkage, aging, and market conditions to keep asset values aligned with economic reality.

Inventory loses value through four primary channels: product obsolescence from shifting demand or technology cycles, physical damage or spoilage during storage and transit, market price declines driven by competition, and excess stock that accumulates carrying costs over time.

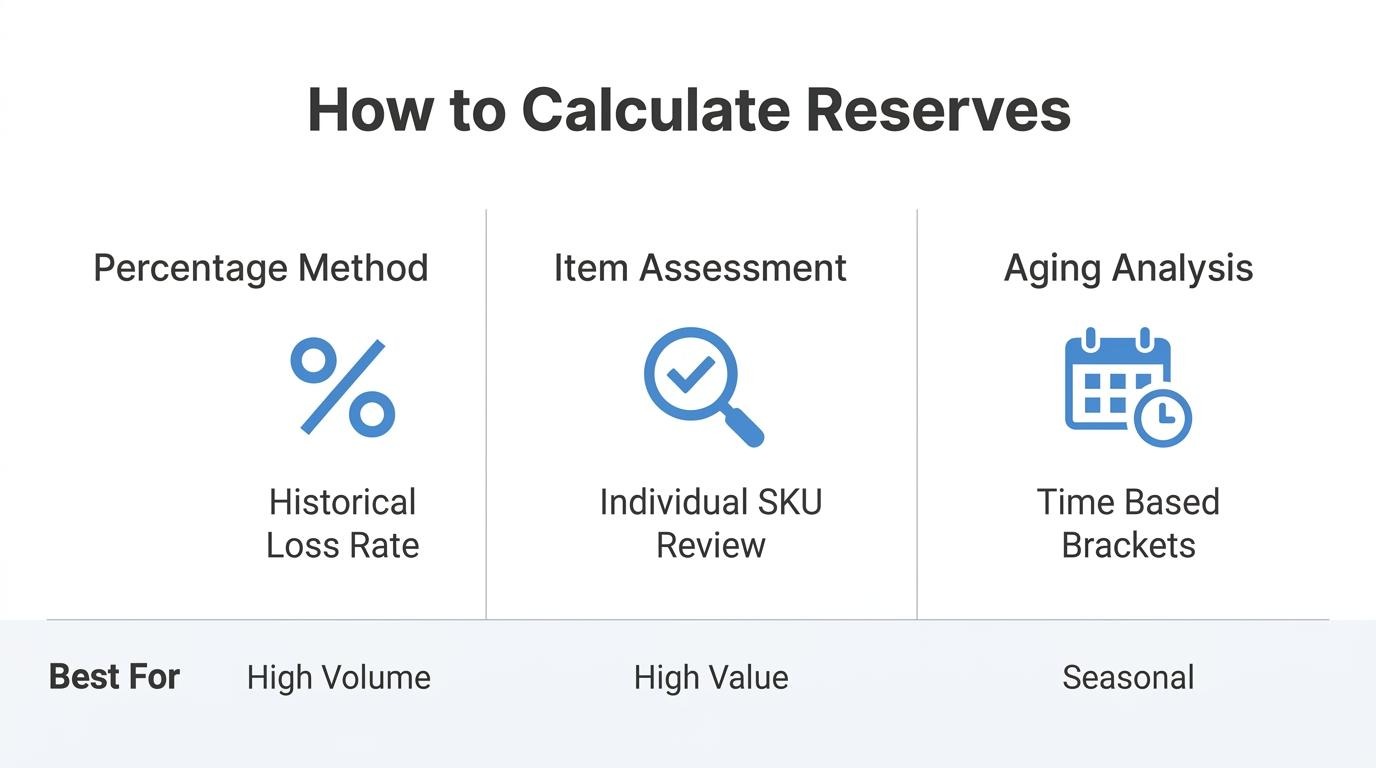

Three calculation methods serve different business needs. The percentage-of-sales approach applies historical loss rates to current gross inventory. Item-by-item assessment evaluates individual SKUs against net realizable value. Aging analysis assigns escalating reserve percentages to stock held beyond defined time brackets.

U.S. GAAP (ASC 330) and IFRS (IAS 2) diverge on a critical point: GAAP prohibits reversing inventory write-downs once recorded, while IFRS permits reversals when recovery conditions arise. This distinction shapes how conservatively businesses must treat valuation adjustments across jurisdictions.

Real-time inventory visibility across online and in-store channels replaces conservative guesswork with data-driven reserve estimates, reducing the discrepancies that force businesses to over-reserve against unknown gaps.

Businesses need an inventory reserve to prevent financial statements from overstating the true value of stock on hand. Without this contra-asset account, balance sheets would carry inventory at full cost even when portions are likely unsellable due to obsolescence, shrinkage, damage, or market decline.

The scale of potential loss is significant. According to the National Retail Federation's 2023 National Retail Security Survey, the average shrink percentage of 1.6% of total retail sales represented $112.1 billion in losses for U.S. retailers in 2022. These losses do not announce themselves individually; they accumulate across thousands of SKUs over months, making proactive reserving essential.

Several conditions make inventory reserves necessary:

For any brand managing meaningful inventory volume, the reserve serves as a financial buffer that aligns reported assets with economic reality. Skipping this step risks misleading investors, triggering audit issues, and distorting profitability metrics. Improving inventory visibility through integrated platforms helps companies reduce costly overstock, which directly lowers the need for large obsolescence reserves.

Understanding why reserves exist sets the stage for how they function in daily accounting practice.

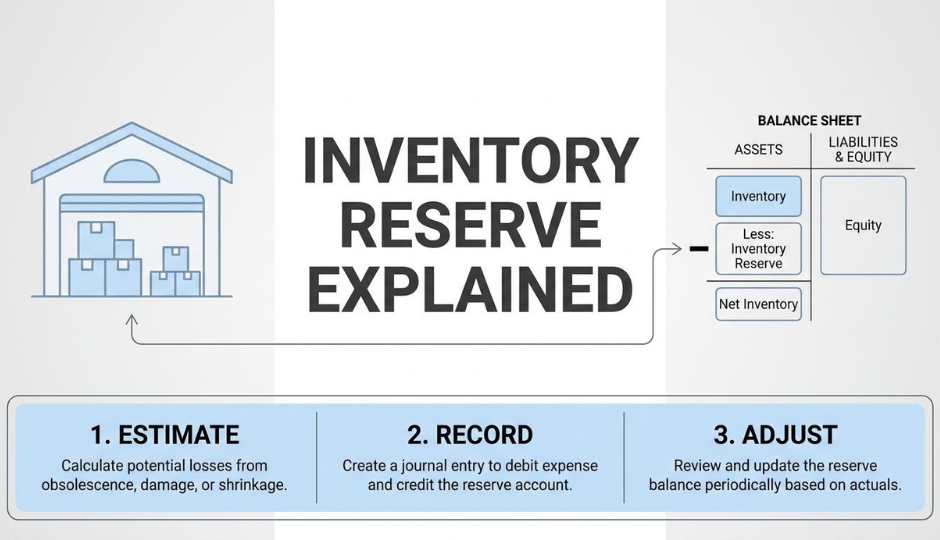

An inventory reserve works in practice through a three-step cycle: estimating the initial reserve amount, recording journal entries, and adjusting the balance over time as conditions change.

The initial reserve estimate is calculated by identifying inventory likely to lose value and applying an appropriate percentage or dollar reduction to gross inventory. An inventory reserve functions as an asset contra account, used to write down inventory value for items expected to be written down due to obsolescence, spoilage, or theft, even when specific items have not yet been identified.

Two common estimation approaches include:

Once calculated, the initial creation involves a debit to Cost of Goods Sold (COGS) and a credit to the inventory reserve contra-asset account on the balance sheet.

Journal entries for an inventory reserve are recorded by debiting COGS and crediting the inventory reserve contra-asset account when establishing or increasing the reserve. According to Abby Jenkins, Product Marketing Manager at NetSuite, "when an inventory reserve is created on the balance sheet, an expense of the same amount is included in cost of goods sold (COGS) on the income statement," effectively recognizing a future cost today.

When an identifiable reduction occurs later (such as confirmed obsolescence or disposal), the reserve account is debited and the inventory asset account is credited.

For example, a company with $1,000,000 in gross inventory applying a 3% reserve would record:

This process ensures inventory is stated at the lower of cost or net realizable value, which is particularly critical given that approximately 58% of retail brands and D2C manufacturers report inventory accuracy levels below 80%.

The reserve is adjusted over time by reviewing inventory balances each reporting period and revising the estimate based on current conditions. According to PwC, inventory balances are adjusted for factors including shrinkage, aging, obsolescence, seasonality, and permanent markdown accruals to ensure financial accuracy.

If actual losses exceed the reserve, the company increases it with additional COGS charges. If conditions improve, the reserve may be partially released. Inaccurate reserving in either direction distorts financial health; excessive reserves create hidden cushions that may signal earnings manipulation, while inadequate reserves overstate assets on the balance sheet.

Consistent review methodology matters more than precision in any single quarter, because defensible reserves depend on documented assumptions and repeatable processes rather than one-time estimates.

With reserve mechanics established, understanding the root causes of inventory value loss helps businesses set more accurate estimates from the start.

Inventory loses value due to obsolescence, physical damage, market price declines, and excess stock accumulation. Each factor triggers a different type of reserve adjustment.

Obsolescence occurs when inventory becomes outdated, unsellable, or functionally irrelevant before it can be sold. Technology upgrades, shifting consumer preferences, and regulatory changes all accelerate this process. According to Aurora Training Advantage, an obsolescence reserve is an allowance account used to reduce reported inventory value to reflect items that may become outdated or lose value before sale. Products with short innovation cycles, such as electronics or seasonal fashion, face the highest obsolescence risk and typically require larger reserve percentages.

Physical damage or spoilage reduces inventory value when products become unsellable due to breakage, contamination, or expiration. Industries handling fragile items and perishable goods are particularly vulnerable. Warehouse mishandling, improper storage conditions, and transit incidents compound these losses. Inventory shrinkage from such causes is primarily attributed to factors including administrative errors alongside theft, according to Pallite. For merchants selling across multiple channels, inconsistent storage standards between fulfillment locations often magnify spoilage rates beyond what single-warehouse operations experience.

Market price decline causes inventory to lose value when the current selling price drops below the recorded cost. Increased competition, reduced consumer demand, or commodity price shifts all drive this gap. Accounting standards require a reserve adjustment to align with the lower of cost or market principle, ensuring inventory is not overstated on the balance sheet. This scenario is especially common in commoditized categories where price erosion happens quickly and unpredictably.

Excess or slow-moving stock loses value through carrying costs and declining sellability over time. Overpurchasing, inaccurate demand forecasting, and poor assortment planning create surplus that ties up capital. Under LIFO valuation during inflationary periods, these older units reflect inflated costs that increase COGS deductions and defer taxable income. Identifying slow-moving SKUs early remains one of the most practical ways to minimize reserve requirements and preserve working capital.

Understanding these value-loss triggers clarifies how reserve calculations are determined.

You calculate an inventory reserve using historical loss data, individual SKU evaluation, or time-based aging categories. The three primary methods are the percentage-of-sales method, the item-by-item assessment method, and the aging analysis method.

The percentage-of-sales method estimates reserves by tracking the percentage of inventories that were never sold or spoiled in past fiscal periods, then applying that historical rate to current gross inventory. According to AccountingTools, a company with $1,000,000 in gross inventory using a 3% historical loss rate would record a $30,000 debit to cost of goods sold and a $30,000 credit to the inventory reserve contra account.

This approach works best for businesses with consistent, predictable loss patterns across reporting periods. For brands managing high SKU counts, the percentage-of-sales method offers a practical starting point before layering in more granular analysis.

The item-by-item assessment method evaluates each SKU individually to determine whether its net realizable value has fallen below recorded cost. The assessor reviews factors specific to each product:

This granular approach produces the most defensible reserve estimates because it ties each adjustment to identifiable evidence rather than broad assumptions. However, it demands significant time and data access, making it most practical for businesses with smaller, high-value inventories or for validating reserves flagged by other methods.

The aging analysis method categorizes stock by the length of time it has been held, with increasing reserve percentages applied to older categories to reflect higher risks of obsolescence. According to PwC's inventory accounting guidance, aging analysis assigns escalating write-down rates as inventory ages through defined time brackets.

A typical structure applies progressively higher reserve rates:

Aging analysis is particularly effective for retailers and e-commerce brands dealing with seasonal or trend-driven products where holding time directly correlates with loss probability. Understanding these calculation methods helps determine where inventory reserves appear on financial statements.

An inventory reserve appears on the balance sheet as a contra-asset account that reduces gross inventory value, while its corresponding expense appears on the income statement within cost of goods sold.

The inventory reserve sits directly beneath the inventory line on the balance sheet, offsetting total inventory to show net realizable value. On the income statement, the expense charged when creating or increasing the reserve flows through COGS, reducing reported gross profit for that period. This dual placement means any adjustment to the reserve simultaneously affects both asset valuation and profitability metrics.

The choice of inventory costing method influences how these figures interact with taxable income. According to research from the Tax Foundation, choosing the LIFO inventory method generally lowers both taxable income and financial income during periods of rising costs, while FIFO typically raises both. This distinction matters because the reserve calculation builds on whichever cost basis the company has elected.

Consistency in how reserves are estimated is critical to financial statement reliability. Inconsistent methodology or unsupported assumptions in estimating obsolescence can lead to material misstatements of inventory and cost of goods sold, presenting significant audit risk. Under-reserving creates artificially inflated assets on the balance sheet, while over-reserving depresses earnings in ways that may signal earnings manipulation to auditors and investors.

For brands operating across multiple channels, getting the reserve right requires accurate, real-time inventory data feeding into both statements simultaneously.

An inventory reserve relates to GAAP and IFRS through each framework's rules on valuation measurement and write-down reversals. The key differences involve cost formulas, lower-of-cost thresholds, and whether previously recorded write-downs can be reversed.

U.S. GAAP (ASC 330) requires inventory to be stated at the lower of cost or net realizable value. Once a write-down is recorded, GAAP generally prohibits reversing it, even if market conditions improve. U.S. GAAP also permits different cost formulas across inventory categories without requiring uniformity.

IFRS (IAS 2) takes a different approach. According to an RSM US comparison of the two frameworks, IFRS allows inventory write-downs to be reversed up to the amount of previous write-downs if the reasons for the write-down cease to exist; U.S. GAAP does not permit this reversal. IFRS also requires the same cost formula for all inventories having a similar nature and use to the entity, while U.S. GAAP does not impose such a requirement.

This reversal distinction matters for reserve management. Under GAAP, a recorded inventory reserve is permanent. Under IFRS, reserves can be partially unwound when recovery occurs, which directly affects reported earnings in subsequent periods. For businesses operating across jurisdictions, understanding which standard governs their financial statements determines how conservatively they must treat inventory valuation adjustments over time.

The difference between an inventory reserve and a write-off is one of timing and certainty. A reserve is a proactive estimate recorded before specific losses are confirmed, while a write-off is a reactive removal of inventory value after a loss is identified and verified.

An inventory reserve reduces the carrying value of stock on the balance sheet through a contra-asset account, anticipating future losses from obsolescence, shrinkage, or spoilage. The inventory itself remains on the books at a reduced net value. A write-off, by contrast, eliminates the asset entirely; the specific items are confirmed as worthless and removed from inventory records.

This distinction matters for financial planning. Reserves smooth earnings impact across periods by recognizing expected losses gradually. Write-offs create a sudden, concentrated hit to profitability in a single reporting period. According to Alexander Jarvis, healthy e-commerce inventory write-off rates are typically below 1–2% of total inventory, measuring stock discarded due to damage, obsolescence, or theft.

For brands managing large product catalogs, maintaining adequate reserves prevents the financial shock of unexpected write-offs. The reserve acts as a buffer that has already absorbed anticipated value loss incrementally, so when the actual write-off occurs, much of the expense has already flowed through cost of goods sold. Brands that skip the reserve step often face sudden margin compression when damaged or obsolete stock finally requires removal.

Understanding how reserves and write-offs interact with tax reporting adds another layer of complexity, particularly around inventory valuation methods and their effect on taxable income.

Inventory reserve affects tax reporting by influencing taxable income through its impact on Cost of Goods Sold (COGS) and the inventory costing method a business selects.

When a company increases its inventory reserve, the corresponding debit to COGS raises total expenses on the income statement, which reduces taxable income for that reporting period. The inventory valuation method chosen amplifies or diminishes this effect. According to IRS documentation, the LIFO reserve represents the difference between ending inventory valued using LIFO and ending inventory valued at current year cost; this difference is used to calculate taxable income and defer taxes.

During inflationary periods, LIFO reflects inflated costs that increase COGS deductions, effectively deferring taxable income to future periods. FIFO, by contrast, typically raises both taxable income and financial income during rising costs because older, lower-cost inventory flows to COGS first. The costing method a business selects determines how reserve adjustments translate into actual tax liability.

For scaling brands managing inventory across multiple channels, the accuracy of reserve estimates directly determines whether tax filings overstate or understate deductions. Overly aggressive reserves inflate COGS and under-report income; inadequate reserves do the opposite. Either scenario creates audit risk with the IRS.

Understanding the tax implications of inventory reserves requires careful coordination between accounting methodology and tax strategy to avoid compliance issues.

Common mistakes when managing inventory reserves include under-reserving, using inconsistent estimation methods, and misclassifying the reserve on financial statements. These errors distort reported asset values and create audit risk.

One frequent misconception involves classification. A common Google PAA question, "Is inventory reserve a current asset?", reveals widespread confusion; the inventory reserve is a contra-asset account that reduces reported inventory value, not a standalone asset.

Additional pitfalls include:

For scaling brands managing inventory across multiple channels, these errors compound quickly when stock data lives in disconnected systems.

Accurate inventory data reduces reserve guesswork across channels by replacing manual estimations with real-time stock visibility. Unified systems and integrated warehouse tools minimize the discrepancies that force businesses to over-reserve.

When online and in-store inventory lives in one system, reserve estimation errors drop because stock counts reflect actual quantities across every sales channel simultaneously. A unified inventory system improves tracking and order fulfillment accuracy by using real-time stock visibility, according to Fulfillment IQ. Instead of reconciling separate databases where discrepancies accumulate unnoticed, a single source of truth exposes shrinkage, damage, and slow-moving stock as it occurs. This precision means reserve percentages can be based on verified data rather than conservative guesses designed to cover unknown gaps. For brands selling across online storefronts, marketplaces, and physical retail, consolidating inventory into one system is one of the most effective ways to tighten reserve accuracy.

The key takeaways about inventory reserves are:

Brands operating at scale benefit most when their inventory, CRM, and sales data resolve to one record, turning reserve accounting from guesswork into a data-driven exercise.